A debit card combines features consistent with a credit and ATM card for easy access to funds in a traditional bank checking account. More people are moving away from cash in favor of managing finances with some form of “plastic.”

The benefit of a debit card over credit is there is no accrual of interest; the funds accessed belong to you. While this is considered an advantage, there are also downsides, particularly if you overspend from the account. This is when fees and charges and possible penalties can be imposed, which can be costly.

Fortunately, if a card is lost or stolen, the financial institution will take steps to either freeze the card or close the account to avoid fraudulent charges from accruing. When using cash, there’s minimal likelihood for recovery if it goes missing since often there’s no paper trail leading to its whereabouts.

Before obtaining a debit card or using one, it’s essential to learn what the card is, how it works, and weigh the advantages and downsides associated with your particular situation.

The Fundamentals of a Debit Card

Debit cards allow payments to be withdrawn from a traditional checking account instead of carrying cash. Please visit kredittkortinfo.no/debetkort/ for details on what a debit card is.

While cash will never lose favor since it is accepted everywhere, never denied, and is international, it’s also the least secure and safe to bring with you in any given circumstance.

A debit card is the next best financial solution since the funds are your own, but you can rest assured that if the card is lost or stolen, a bank will cease use of the account, freezing the funds and closing the card.

There are no interest or associated fees and charges for using the card comparable to those that would be imposed for using a credit card. The funds are immediately taken from your personal funds with no pending invoice that must be repaid.

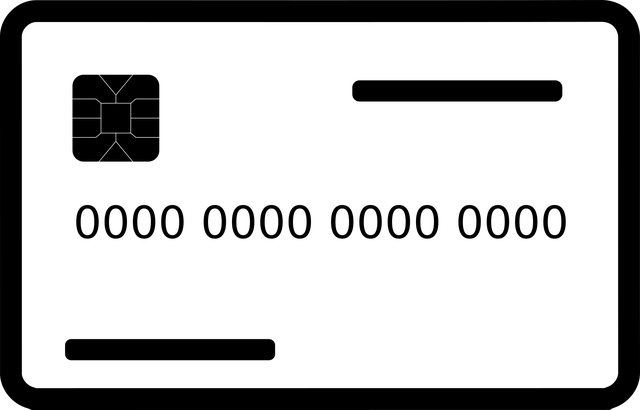

Debit cards are similar in appearance to a credit card and can be confused for these. They have an account number across the face with the account holder’s name and an expiration date.

The card will have a “smart chip” for straightforward use along with the payment network logo like “Master card.”

The back of the card will show the security code. The primary difference between a debit card and other financial tools is that you’ll be using your own funds instead of borrowing or owing money to a company or credit card issuer.

That means there will be no accrual of interest or minimal amount due to contend with if you use a debit card. The funds will be there and available to you at your leisure, with no balance due when using it.

What Is the Best Way to Get a Debit Card

Getting a debit card is as easy as opening a new bank account. Often, the financial institution will inquire whether you want to receive a debit card on the account or if you decline to do so.

The protection offered by the bank with debit cards is the greatest for security and safety, something not guaranteed when using cash. If the card goes missing, either by misplacing it or having it stolen, the financial institution will freeze the account or close the card.

Protection when using cash for any sort of expense is minimal to no possibility for recovery. Here is the best way to get a debit card to ensure you’re not the victim of fraud.

Sign on for a traditional bank checking account

As a rule, most people agree to take a debit card when opening a traditional bank checking account. These allow simple access to your funds when using an ATM in your local area or any location around the world.

Typically, you can receive a debit account immediately when signing on to check with any financial entity in person. When applying with an institution online, you can expect a few day’s turnaround to receive the card.

As the cardholder, you’ll need to assign a specific PIN- personal identification number for the most security with the account.

Card activation

A priority when receiving a debit card is to activate it. You won’t be able to use its benefits until it’s set up. This is a primary part of safety and security with this financial tool.

Usually, card activation is relatively straightforward and simple, with the capability to do so using the bank’s website, an ATM kiosk, or by using the phone number designated on the debit card. This will require inputting some sensitive details to ensure there’s no fraud involved in the activation.

This will speak to the bank that the person with the card is the genuine bank account holder and allows them to move forward with the process. You’ll be asked to assign a PIN- personal identification number to protect its use further.

Card use

After the initial steps, you should be able to access the card’s benefits and use it with most vendors or in the online medium. You can use the card to make quick and easy ATM withdrawals, shop in person and online, or submit automatic payments with creditors for balances due.

A major convenience of a debit card is its versatility to obtain cash, transfer funds, make deposits, or simply assess your current balance, frequent activities, and overall activity, all of which can be achieved with a reliable ATM.

Before stepping away from an ATM, pay attention to whether the machine removed your sensitive details before another person steps up to use the ATM.

As a rule, it’s wise to sign on with a banking institution that reimburses for specific fees and charges or doesn’t charge these from the start, including foreign transaction fees, if you travel overseas often.

Some merchants will allow debit users to receive cash back with PIN purchases instead of forcing an ATM withdrawal to save time and effort when shopping. When agreeing to get cash back from a merchant, small fees can be associated with these transactions.

Many debit cardholders will use their card for auto pay with most creditors. However, this requires divulging sensitive personal and financial details with permission to withdraw funds from the banking account on a continuous basis.

As the cardholder, you can authorize the amount that comes out of the account since some account payments, like utility payments, will vary each month.

Spending

A priority with a debit card is to remain within your account spending limits. While it’s your money in the account, in order to get more funds with a bank checking account, you need to deposit more money. When overspending, you expose yourself to hefty fees and charges for over drafting the account.

This can have a significant impact on your financial standing, particularly if you use the debit card to auto pay monthly expenditures. If you don’t have enough money in your account to pay the overdue debt, default can occur on accounts sometimes without you being aware until it’s too late to spare your credit.

It’s wise to constantly review your bank checking account to be fully aware of the balance, pay attention when funds are being withdrawn and when money goes in.

You’ll be a step ahead if you need to top off the balance to keep the auto pay running smoothly for the varied creditors with whom you participate in the program.

Final Thought

Debit cards are a financial tool people use to access cash in their bank checking account to make purchases online or in-person, for travel, buy fuel or dine, plus use when signing on for auto pay with creditors to satisfy debt.

The benefit of a debit over a credit card is the money is already yours. Once you use it, there won’t be interest accrual or fees and charges; you don’t have to pay it back.